If I were a business owner, I would love it if my products were on the Price is Right. Aside from the brand recognition, it would help me achieve price optimization, or the ideal price for my products.

If you’re unfamiliar with the Price is Right, it’s a game show where contestants guess the price of different household items. It’s fascinating because you see what people would pay for everyday products. As a business owner, it helps you understand the value of your products and how much you should charge for them.

Free: 3 Master Strategies for Raising Your Prices

Use this guide to help you decide when and how to increase what you charge, and improve your bottom line.

Save NowThis post will break down price optimization and how your business can achieve it. We’ll discuss how to optimize pricing and different pricing optimization models. By the end of this post, you won’t need Drew Carey to tell you if the price is right; you’ll have everything you need to position your business for success.

What Is Price Optimization?

Price optimization is the process of analyzing data to determine the best price for your products and services. It evaluates customer information, business resources, and other data points to establish a price that attracts customers and drives revenue for your business.

Here are some of the variables that pricing optimization accounts for:

- Customer Information: Surveys, Reviews, Product Usage

- Demographics: Location, Age, Target Audience

- Business Resources: Inventory, Supply Chains, Personnel

- Operating Costs: Workspaces, Tools, Supplies

- Sales Data: Previous Sales, Demand, Forecasting

- Competition: Competitor Pricing

Keep in mind that pricing optimization isn’t just for products. These factors affect service-based businesses, which use pricing optimization to determine the best price for their offers. While the variables influencing price may differ, the process is the same.

Now, let’s review a few scenarios where you’ll optimize product pricing.

Product Pricing Optimization

Here are three cases where pricing optimization is necessary to determine the ideal price for your products or services.

Base Pricing

Base pricing refers to your product’s starting price. It’s the default price without any sales or promotions attached. Your base pricing is important because it represents the value of your product. It should align with customer demand and generate adequate revenue for your business.

Promotional Prices

Sales are a great way to increase revenue, and pricing optimization helps determine how much of a discount to provide. It’ll ensure you’re lowering prices enough to attract more customers and generating enough revenue for your sale to be worth it. A good sale should make customers happy while increasing profits for your business.

Discounted Prices

You may have to negotiate some of your sales if you work in a service-based industry. Pricing optimization helps you determine the lowest price you can charge while making money for your business. It can also help you close a deal and secure a high-value customer who consistently shops at your company.

3 Master Strategies for Raising Your Prices

Here’s what you need to keep in mind.

What is an optimal pricing strategy?

Not every business earns the same. Companies like Nike sell products online and in stores. Businesses like Spotify sell subscription services online. And, your local mechanic makes their living on recurring purchases, like inspections and oil changes.

The point is: Yyour optimal pricing strategy differs depending on your industry. It’s also affected by your customer base, the size of your business, and the resources you have at your disposal. What works well for one company may not be effective for another. Finding an optimal product price takes time and may require some adjustments to get things right.

Let’s discuss how you can optimize pricing at your business using the steps in the next section.

How to Optimize Pricing

Here are five steps to optimize the price of your products and services.

Step 1: Do your research.

The best place to start is with data. Dive into your CRM, customer reviews, and website reporting to learn as much as possible about your customers. You should also perform a market analysis to research competitors in your area and quantify factors like supply and demand and customer perception. That will help you see what other businesses charge for similar products and what your customers think about those prices.

You should also look at historical data like sales performance and average customer lifetime value. If your products aren’t selling as well as you would expect, this information provides insight into buyer frequency and the average price of each purchase.

Finally, you should also consider branding. If you’re competing against luxury or big-box brands, they might charge more because of the brand value behind their offers. Identifying this is important because it can be a huge marketing opportunity for your business. If you sell the same products at a lower price, you can stand out from your competitors.

Step 2: Define what and how you will sell.

Customers want to know what they’re paying for, or your “value metric.” It’s what you sell and how you sell it to customers.

For example, Amazon Prime is a subscription service. Customers pay a fee each month, and in return, they get exclusive perks like free shipping and Prime Video. Customers pay for Amazon Prime because the price matches the value metric. They feel like they are getting a good deal by paying this additional fee.

Identifying your value metric is important because it shows you what customers value about your product and what you can charge for it. Service-based businesses like landscapers might rely on their quality, while e-commerce shops might focus on competitive pricing. It all depends on what you do best and what customers think is valuable.

Step 3: Create pricing tiers.

Pricing tiers are like levels for your products and services. The more premium the product, the more you charge for it. It’s a common strategy for service-based businesses like car washes and dog groomers.

Here’s an example from a local car wash. Notice how it includes different tiers with unique features for each. As you increase in price, you get more services and perks:

Pricing tiers give customers options. People looking for a basic service can purchase a lower tier, while customers shopping for a premium product can choose a higher one. This flexibility increases your chances of selling because it addresses different customer needs.

Step 4: Communicate with your customers.

Once you’ve settled on a pricing strategy, it’s critical to communicate this change to your customers — especially if you’re increasing prices. No one wants to pay more for a product, but unfortunately, this is a reality for some businesses. Knowing how to effectively tell your customers about a price increase is key to having a successful pricing model.

While we have a complete guide here, below are some tips for telling customers about a price change:

- Be upfront and honest about why you are changing prices.

- Be proactive; give customers plenty of notice.

- Stand by your decision. Some customers are going to be upset.

- Roll out new costs slowly.

- Create additional value where possible.

Step 5: Adjust and monitor.

Once you’ve communicated this change, it’s time to implement your new pricing plan.

But, the work doesn’t stop here. It’s time to monitor your changes to see if they have the intended result. If so, great! Keep an eye on things going forward and look for other areas of your pricing model to optimize.

If you aren’t experiencing success, review your customer data. Look at recent reviews and collect customer feedback. If your most loyal customers are making fewer purchases, reach out to them to see why things have changed. They might have ideas for improving your prices to make them more appealing.

The most important part is that you shouldn’t get discouraged. Finding the best price for your products and services may take time. Many successful companies have gone through years of testing and are still trying to optimize their pricing plan. Be patient, collect feedback, and make small changes until you see the results you’re looking for.

Let’s review a few different strategies you can use to optimize pricing at your business.

3 Master Strategies for Raising Your Prices

Here’s what you need to keep in mind.

Pricing Optimization Models

Here are three common price optimization models for small businesses. These strategies will help you determine your value metric and the best way to sell your products.

1. Markup Pricing

Markup pricing, or cost-plus pricing, means you add a fixed percentage to your production costs. You determine what it costs to make the product, then add a fee to ensure your business returns a profit.

For example, if I sold beauty products, I would calculate the cost of building and shipping each product. Then, I would mark up the pricing to account for overhead costs like resources, employees, etc. Every time I sold a product, I would make a profit.

The challenge with this approach is flexibility. If you overcharge, customers won’t buy your products. If you undercharge, you’ll miss out on an opportunity to grow your business. With this strategy, finding the best price may take time to get things right.

2. Captive Product Pricing

Captive product pricing means selling products that rely on other products.

The iPhone is a great example. Apple changed the charging cord not because it improved the phone but because it forced users to buy new Apple accessories.

Printers are another example. Most printers only have one type of ink cartridge that only works with one machine. You have to buy that specific cartridge if you want to keep using your printer.

This strategy is effective if you want to generate recurring purchases for your business. The challenge is offering a product or service that’s worth buying over and over again. Customers who find a cheaper alternative might abandon your brand if they don’t love your product.

3. Competition-Based Pricing

Competition-based pricing means basing your pricing on competitors in your industry. You might charge something similar or decrease your pricing to make your business stand out.

Another option is to charge more for your products. Why? Because it positions your brand as a premium alternative to competitors. That implies your product is higher quality or more exclusive than other brands.

A classic example is Nike. You can find comparable products sold by brands like Under Armour and Rebook. But, as a Nike customer, I can tell you that its sweatpants are better than those of other brands. They’re comfier, and they’re made of a stronger material. As a customer, I don’t mind paying more for Nike because it’s a better product than the alternatives.

These models are the most popular ways to price a product – but there are more strategies beyond these three. Here’s a list of pricing optimization models and a quick description of each.

- Hourly: You charge customers a fixed rate by the hour, and you’re paid based on the time you spend working.

- Demand: You adjust your prices based on customer demand. The greater the demand, the higher the price.

- Bundling: You package products together and then sell them at a reduced price.

- Dynamic: You increase prices as more customers purchase your product. For example, airline tickets increase when fewer seats are available on the plane.

- Psychological: Your price is designed to elicit a response from customers. For instance, charging more suggests it’s a higher quality product.

- Freemium: You offer your product for free, then sell upgrades and add-ons over time.

- Price Skimming: You mark up your prices but then slowly lower them over time.

- Odd-Even: You use an odd number for pricing ($5.99) or round it to the nearest tenth ($6.00). The odd number suggests a bargain, while the even number implies a premium offer.

- Penetration: You offer your product at a much lower price than the rest of your marketplace.

- Loss Leader: You create a sale for one product that attracts customers to your business. Those customers then purchase additional products, which evens out the loss you take on the sale.

Before we wrap up, let’s look at a company that successfully pulled off a price change.

Price Optimization Example

Netflix is one of the most successful brands in the world, and it’s come a long way since starting as a small DVD rental company.

Over the years, Netflix has grown dramatically from a tiny subscription service to a global, multi-billion-dollar brand. It has adapted its prices to keep up with changes in its industry, new products, and customer behavior. For example, in 2007, Netflix launched its streaming service, which created a whole new pricing model. Customers fell in love with streaming videos online, and now it’s the company’s core value metric.

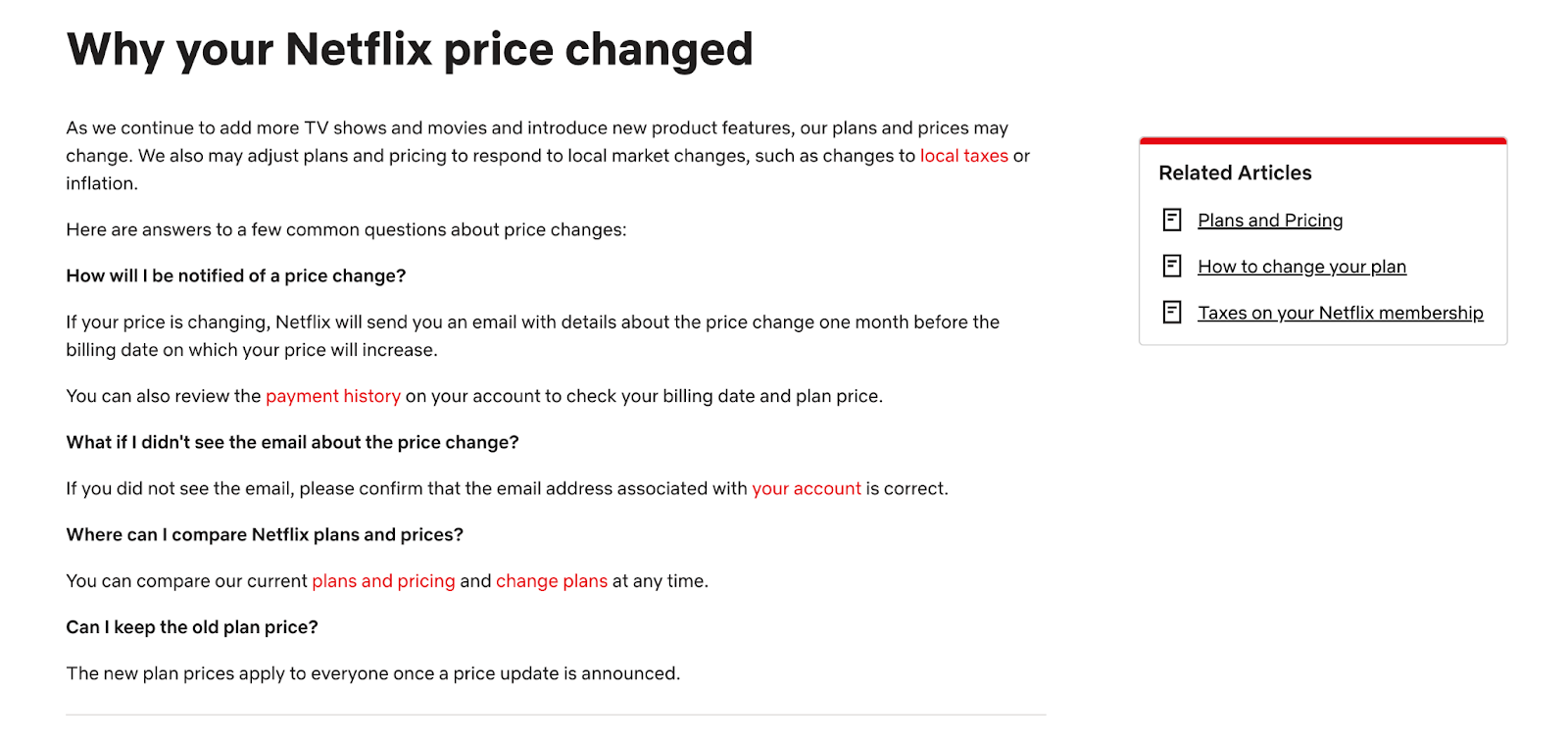

Most recently, Netflix raised the price of its Basic plan from $10/month to $12/month and its Premium plan from $20/month to $23/month. To communicate this change, Netflix posted this FAQ page and distributed it to its customers. It also sent emails notifying customers about potential price changes and gave them resources to change or cancel their service.

To be clear, customers didn’t love this change, but it didn’t hurt Netflix as a business. In fact, membership continues to grow, and most customers accepted the price changes rather than cancel or change plans. Netflix got ahead of the news and gave customers plenty of notice, and most people accepted it and moved on. The company initially received some expected backlash, but this blew over, and Netflix continues to turn a profit.

Love or hate this change, here’s what Netflix did well:

- The company was proactive and gave customers ample time to plan for the price change.

- Netflix was honest about why it was making this change. It cited “to add more TV shows and movies” and mentioned that some changes may be a reaction to local taxes and inflation.

- Netflix provided resources for customers to learn why it was making this change and what they could do to update their subscriptions.

Is the Price Right?

If you want your business to succeed, you have to sell your products and services at the right price. Charge too much, and customers won’t be interested in your business. Charge too little, and you won’t make any money.

Finding the right balance means researching your customers and testing new models. Use the tips in this post to optimize your pricing strategy and position your business for long-term success.

3 Master Strategies for Raising Your Prices

Here’s what you need to keep in mind.